One Big Beautiful Bill Act

Overview

On July 4, 2025, the One Big Beautiful Bill Act became law, bringing major updates to federal student aid programs. Starting July 1, 2026, these changes will begin to reshape how students and families finance higher education. We are currently reviewing the legislation and will continue to provide updates as the U.S. Department of Education and other authorities release additional guidance.

Below is a summary of what we know at this time, how these updates may affect you, and steps you can take to start preparing. This information is intended to help students and families understand and navigate the upcoming changes to federal student aid. It reflects our good‑faith interpretation of what to expect.

Federal Student Aid Changes for the 2026-27 Aid Year

- Any student who has an SAI that is twice the maximum Pell will not be Pell eligible.

- Students receiving scholarships that cover their full cost of attendance won’t be eligible for Pell.

The new regulations bring about several important modifications to the federal student loan options. Here are the most critical updates effective July 1, 2026:

Loan Limits

|

Loan Type |

Current Annual Limit (25/26 Academic Year) |

Current Aggregate Limit |

New Annual Limit |

New Aggregate Limit |

|

Undergraduate Subsidized |

Freshman-$3,500 Sophomore $4,500 Junior/Senior-$5,500 |

$23,000 |

Unchanged |

Unchanged |

|

Undergraduate Unsubsidized for Dependent Students |

Freshman-$2,000 Sophomore $2,000 Junior/Senior-$2,000 |

$31,000 |

Unchanged |

Unchanged |

|

Undergraduate Unsubsidized for Independent Students |

Freshman-$6,000 Sophomore $6,000 Junior/Senior-$7,000 |

$57,500 |

Unchanged |

Unchanged |

|

Graduate Unsubsidized Loans |

$20,500 |

$138,500 (includes undergraduate borrowing) |

$20,500 |

$100,000 (Graduate level loans only) |

|

Graduate PLUS Loans |

Up to the cost of attendance minus other sources of financial aid |

None |

Eliminated |

Eliminated |

|

Parent PLUS Loans |

Up to the cost of attendance minus other sources of financial aid |

None |

$20,000 per dependent student |

$65,000 per dependent student |

- If a parent is denied a Parent Plus loan, a dependent student can borrow up to an additional $4,000 in unsubsidized loans.

- If a student is not eligible for a subsidized loan, the total annual loan amount for the unsubsidized loan would be the combination of the subsidized and unsubsidized loan. This is dependent on their remaining aggregate loan eligibility.

If you are enrolled less than full-time, your annual loan limit will be prorated based on your enrollment intensity. This means the amount you can borrow in a given year will be proportional to the number of courses you are taking.

- If a borrower has a Federal Direct Loan disbursed before July 1, 2026, while currently enrolled in a credentialed program, the borrower can continue to borrow under current loan limits for three academic years or the remainder of their expected time to credential, whichever is reached first.

- Current Graduate students can finish out their current program under the old loan limits, as well as have access to Graduate PLUS loans until the end of their academic program, or three academic years, whichever is first.

- Current borrowers are defined as those who have borrowed at least one Graduate PLUS or Direct Unsubsidized loan prior to July 1, 2026, and who will remain in the same academic program after July 1, 2026.

- If you switch to a different academic program, even within the same institution, this can place you in a new borrowing category. This means your loan limits and eligibility could be recalculated as if you were a “new borrower,” even if you previously qualified as a “current borrower” under your former program.

- Federal guidance suggests that the definition of “professional degree programs” is being refined and applied within a more precise regulatory framework.

- Initial draft regulations indicate a narrower interpretation of what qualifies as

a “professional degree,” including programs such as:

- Pharmacy (PharmD), Dentistry (DDS or DMD), Veterinary Medicine (DVD), Chiropractic (D.C. or DCM), Law (LLB or J.D.), Medicine (M.D.), Optometry (O.D.), Osteopathic Medicine (D.O.), Podiatry (DPM, D.P., or PodD), Theology (MDiv or MHL) and Clinical Psychology (PsyD or PhD).

**Elizabeth City State University does not currently have any programs that are classified as a professional program. The designation of being a professional program is associated with a higher student loan limit.**

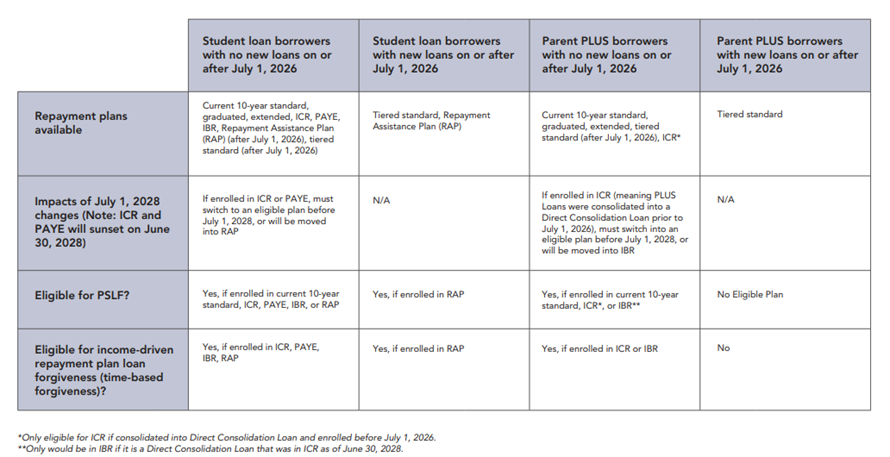

Repayment Plans

Beginning July 1, 2026, federal student loan repayment options will change for both student and parent borrowers. Additionally, important updates will take effect on July 1, 2028, including the sunset of certain income‑driven repayment plans. Below is a clear overview to help students, families, and borrowers understand what to expect based on the type and timing of their loans.

Loan Disbursement Changes Effective July 1st 2026

Direct Loan Enrollment Status & Disbursement Policy

We want you to understand how your enrollment level affects your federal Direct Loans. Here’s a clear explanation of how our school handles changes to your class schedule.

Federal rules require schools to check your enrollment status (full‑time, three‑quarter‑time, half‑time, etc.) each time your loan is disbursed. If you’re enrolled less than full‑time at that moment, your loan amount may be reduced.

If you increase your enrollment level after your loan has already been disbursed for the term:

- We will not issue an additional loan disbursement for that same term.

- Your enrollment will be reviewed again at your next scheduled disbursement, usually the next semester.

- If you qualify for more loan funds at that time, you may receive the additional amount then.

If you decrease your enrollment level after your loan has already been disbursed:

- We will not reduce your loan for that term, unless required by federal rules like Return of Title IV Funds (R2T4).

- This helps prevent unexpected charges on your student account.

- Your loan amount is based on your enrollment at the time of disbursement.

- Adding or dropping classes later in the term usually won’t change that term’s loan amount.

- Your next scheduled disbursement is when any changes may be reflected. If you’re thinking about changing your schedule, we encourage you to talk with the Financial Aid Office so you understand how it may affect your aid.